Application of State Space Representation on Vector Autoregressive (VAR) Models for Forecasting

Article Sidebar

Main Article Content

Abstract

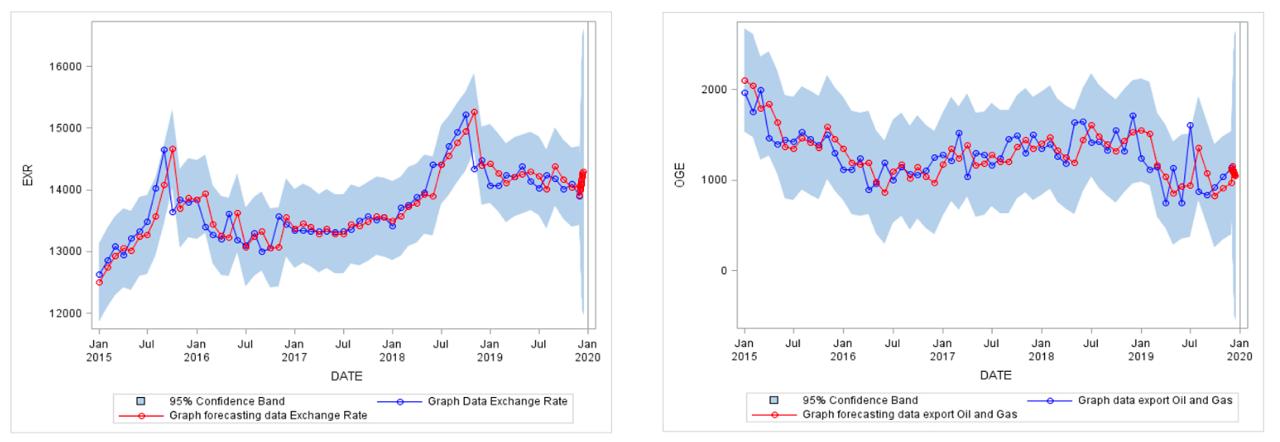

Various analytical techniques are available for modeling multivariate time series data. One such approach is the State Space Model, which can be employed to model this type of data. In this study, the data to be analyzed are data on the Indonesia Rupiah (IDR) exchange rate (ExR) against the US Dollar (USD), oil and gas exports (OGE), money supply (MS) and non-oil and gas exports (non-OGE) from January 2008 to December 2019. The aim of this study is to identify the most suitable state space model for the given data. In this research, the state space method will be applied to multivariate time series data, with the state space represented in the Vector Autoregressive (VAR) model to explore the interrelationships among groups of observed variables. The VAR model is a statistical technique used to analyze the relationships between variables in the dataset, employing the Granger Causality Test. The state space model is utilized to model and forecast multiple interconnected time series, where the variables exhibit dynamic interactions and to examine additional unobserved variables in the time series data. Based on the analysis results and the minimum value of the Akaike Information Criterion (AIC), the optimal VAR model identified is the VAR (6) model. The results of forecasting values using the state space model show that the predicted values and the real values for the state space model are very closed to each other.

Article Details

References

[1] G. Box and G. Jenkins. Time Series Analysis: Forecasting and Control. Holden-Day, San Francisco, 1976.

[2] P. J. Brockwell and R. A. Davis. Time Series: Theory and Methods. Springer Verlag, New York, 2nd edition, 1991.

[3] P. J. Brockwell and R. A. Davis. Introduction to Time Series Analysis and Forecasting. Springer Verlag, New York, 2nd edition, 2002.

[4] R. S. Tsay. Analysis of Financial Time Series. John Wiley & Sons, Inc., New York, 2005.

[5] W. W. S. Wei. Time Series Analysis: Univariate and Multivariate Methods. Pearson Education, New York, 2nd edition, 2006.

[6] J. D. Hamilton. Time Series Analysis. Princeton University Press, New Jersey, 1994.

[7] R. S. Tsay. Multivariate Time Series Analysis. John Wiley & Sons, Inc., New York, 2014.

[8] J. Durbin and S. J. Koopman. Time Series Analysis by State Space Methods. Oxford University Press, Oxford, 2nd edition, 2012.

[9] R. E. Kalman. A new approach to linear filtering and prediction problems. Journal of Basic Engineering, 82(1):35–45, 1960.

[10] R. E. Kalman and R. S. Bucy. New results in linear filtering and prediction theory. Journal of Basic Engineering, 83(3):95–108, 1961.

[11] M. H. A. Davis and R. B. Vinter. Stochastic Modelling and Control. Chapman and Hall, London, 1985.

[12] E. J. Hannan and M. Deistler. The Statistical Theory of Linear Systems. John Wiley and Sons, Inc., New York, 1988.

[13] H. Akaike. Information theory and an extension of the maximum likelihood principle. In B. N. Petrov and F. Csaki, editors, Second International Symposium on Information Theory, pages 267–281, Budapest, 1973. Akademiai Kiado.

[14] H. Akaike. Markovian representation of stochastic processes and its application to the analysis of autoregressive moving average processes. Annals of the Institute of Statistical Mathematics, 26:363–387, 1974.

[15] A. H. Jazwinski. Stochastic Processes and Filtering Theory. Academic Press, New York, 1970.

[16] B. D. O. Anderson and J. B. Moore. Optimal Filtering. Prentice-Hall, Englewood Cliffs, 1979.

[17] M. Aoki and A. Havenner. State space modelling of multiple time series. Econometric Reviews, 10:1–59, 1991.

[18] A. C. Harvey. Forecasting, Structural Time Series Models and the Kalman Filter. Cambridge University Press, Cambridge, 1989.

[19] A. C. Harvey. Time Series Models. Harvester Wheatsheaf, Hemel Hempstead, 2nd edition, 1993.

[20] M. West and J. Harrison. Bayesian Forecasting and Dynamic Models. Springer-Verlag, New York, 2nd edition, 1997.

[21] C.-J. Kim and C. R. Nelson. State-Space Models with Regime Switching, Classical and Gibbs-Sampling Approaches with Applications. MIT Press, Cambridge, MA, 1999.

[22] R. H. Shumway and D. S. Stoffer. Time Series Analysis and Its Applications. Springer-Verlag, New York, NY, 2000.

[23] N. H. Chan. Time Series: Application to Finance. John Wiley and Sons, Inc., New York, 2002.

[24] V. Gomez. Multivariate Time Series with Linear State Space Structure. Springer Verlag, Switzerland, 2016.

[25] H. Akaike. Markovian representation of stochastic processes by canonical variables. SIAM Journal on Control, 13:162–173, 1975.

[26] H. Akaike. Canonical correlation analysis of time series and the use of an information criterion. In R. Mehra and K. Lainiotis, editors, System Identification: Advances and Case Studies. Academic Press, Inc., New York, 1976.

[27] J. Durbin. Introduction to state space time series analysis. In Andrew Harvey, S. J. Koopman, and Neil Shephard, editors, State Space and Unobserved Component Models Theory and Applications. Cambridge University Press, London, 2004.

[28] E. Virginia, J. Ginting, and F. A. M. Elfaki. Application of garch model to forecast data and volatility of share price of energy (study on adaro energy tbk, lq45). International Journal of Energy Economics and Policy, 8(3):131–140, 2018.

[29] Warsono, E. Russel, Wamiliana, Widiarti, and M. Usman. Vector autoregressive with exogenous variable model and its application in modeling and forecasting energy data: Case study of ptba and hrum energy. International Journal of Energy Economics and Policy, 9(2):390–398, 2019.

[30] Warsono, E. Russel, Wamiliana, Widiarti, and M. Usman. Modeling and forecasting by the vector autoregressive moving average model for export of coal and oil data. International Journal of Energy Economics and Policy, 9(4):240–247, 2019.

[31] L. M. Hamzah, S. U. Nabila, E. Russel, M. Usman, E. Virginia, and Wamiliana. Dynamic modeling and forecasting of data export of agriculture commodity by vector autoregressive model. Journal of Southwest Jiaotong University, 55(3):1–10, 2020.

[32] W. Enders. Applied Econometric Time Series. John Wiley and Sons, New York, 4th edition, 2015.

[33] Warsono, E. Russel, A. Putri, Wamiliana, Widiarti, and M. Usman. Dynamic modeling using vector error-correction model studying the relationship among data share price of energy pgas malaysia, akra, indonesia, and ptt pcl-thailand. International Journal of Energy Economics and Policy, 10(2):360–373, 2020.

[34] H. Lütkepohl. New Introduction to Multiple Time Series Analysis. Springer-Verlag, Berlin, 2005.

[35] G. Welch and G. Bishop. An introduction to the kalman filter. Technical report, 2001.