A Hybrid ARIMA–GRU Model for Forecasting Palm Oil Prices at PT Sawit Sumbermas Sarana in Central Kalimantan

Article Sidebar

Main Article Content

Abstract

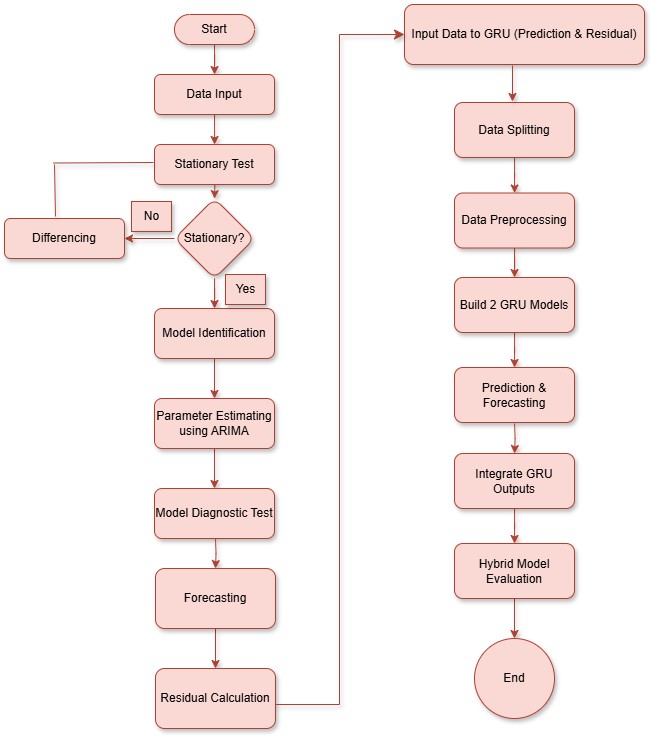

The palm oil industry plays a strategic role in Indonesia's economic landscape. As one of the world’s largest producers, Indonesia holds substantial potential in marketing both crude palm oil (CPO) and palm kernel oil on domestic and international fronts. Palm oil prices consistently correlate with CPO prices, given that the pricing of palm oil is benchmarked against CPO, resulting in market fluctuations. Forecasting future palm oil prices becomes an essential measure in response to this volatility. The ARIMA (AutoRegressive Integrated Moving Average) model has been widely recognized as a reliable method for time series forecasting. Despite its strengths, ARIMA faces challenges in identifying the non-linear components that are often present in real-world data. The Gated Recurrent Unit (GRU) model, which incorporates an update gate and a reset gate, offers an alternative that effectively captures complex non-linear patterns. A hybrid model integrating ARIMA and GRU has therefore been developed with the aim of improving predictive accuracy. This hybrid approach includes two stages: the ARIMA model for initial predictions and a GRU model that processes the residuals from the ARIMA output. In this study, the ARIMA-GRU hybrid model demonstrated strong performance, yielding a Mean Squared Error (MSE) of 868.4690, a Root Mean Squared Error (RMSE) of 29.4698, a Mean Absolute Percentage Error (MAPE) of 0.0117, and an overall accuracy of 99.9824%.

Article Details

References

[1] H. G. Ginting, Z. Azmi, and R. I. Ginting. Jaringan syaraf tiruan dalam peramalan harga jual sawit dengan metode backpropagation. Jurnal Cyber Tech, pages 1–15, 2020.

[2] Kemenperin RI. Tantangan dan prospek hilirisasi sawit nasional analisis: Pembangunan industri, 2021. [Online].

[3] I. E. Pratiwi. The predictors of indonesia’s palm oil export competitiveness: A gravity model approach. Journal of International Studies, 14(3):250–262, 2021.

[4] B. Betrix, H. C. Fajri, and S. S. Rawung. Competitiveness of indonesia’s crude palm oil (cpo) in international markets: Based on database 2018. Journal of International Conference Proceedings, 5(2):106–115, 2022.

[5] N. Salwa, N. Tatsara, R. Amalia, and A. F. Zohra. Peramalan harga bitcoin menggunakan metode arima (autoregressive integrated moving average). Jurnal Data Analitik, 1(1):2131, 2018.

[6] Y. Yu, X. Si, C. Hu, and J. Zhang. A review of recurrent neural networks: Lstm cells and networkarchitectures.Neural Computation, 31(7):1235–1270, 2019.

[7] L. Wiranda and M. Sadikin. Penerapan long short term memory pada data time series untuk memprediksi penjualan produk pt. metiska farma. Jurnal Nasional Pendidikan Teknik Informatika, 8(3):184–196, 2019.

[8] D. Wira. Analisis Fundamenal Saham. Exceed Books, Jakarta, 2nd edition, 2014.

[9] Z. Zhang, X. Pan, T. Jiang, B. Sui, C. Liu, and W. Sun. Monthly and quarterly sea surface temperature prediction based on gated recurrent unit neural network. Journal of Marine Science and Engineering, 8(4), 2020.

[10] H. Wiguna, Y. Nugraha, F. Rizka R, A. Andika, J. I. Kanggrawan, andA.L.Suherman. Kebijakanberbasisdata: Analisis dan prediksi penyebaran covid-19 di jakarta dengan metode autoregressive integrated moving average (arima). Jurnal Sistem Cerdas, 3(2):74–83, 2020.

[11] J. Zhao, Y. Gao, Y. Qu, H. Yin, Y. Liu, and H. Sun. Travel time prediction: Based on gated recurrent unit method and data fusion. IEEE Access, 6:70463–70472, 2018.

[12] U. I. Arfianti, D. C. R. Novitasari, N. Widodo, M. Hafiyusholeh, and W. D. Utami. Sunspot number prediction using gated recurrent unit (gru) algorithm. IJCCS (Indonesian Journal of Computing and Cybernetics Systems), 15(2):141, 2021.

[13] A. M. Sharifi, K. K. Damghani, F. Abdi, and S. Sardar. Predicting the price of bitcoin using hybrid arima and deep learning, 2021.

[14] D. C. Montgomery, L. C. Jennings, and M. Kulahci. Introduction to Time Series Analysis and Forecasting. John Wiley and Sons, New Jersey, 2015.

[15] W. M. Briggs, S. Makridakis, S. C. Wheelwright, R. J. Hyndman, and F. X. Diebold. Forecasting: Methods and applications. Journal of the American Statistical Association, 94(445):345, 1999.

[16] W. W. S. Wei. Time Series Analysis: Univariate and Multivariate Methods. 2nd edition, 2006.

[17] J. E. Hanke and D. Wichern. Business Forecasting, volume 5. 9th edition, 2014.

[18] G. P. Zhang and V. L. Berardi. Time series forecasting with neural network ensembles: An application for exchange rate prediction. Journal of the Operational Research Society, 52(6):652–664, 2001.

[19] L.Zaman,S.Sumpeno,andM.Hariadi. Analisiskinerjalstm dan gru sebagai model generatif untuk tari remo. Jurnal Nasional Teknik Elektro dan Teknologi Informasi, 8(2):142, 2019.

[20] V. R. Prasetyo, M. Mercifia, A. Averina, L. Sunyoto, and Budiarjo. Prediksi rating film pada website imdb menggunakan metode neural network. Jurnal Ilmiah NERO, 7(1):60293, 2022.

[21] S. Sharma, S. Sharma, and A. Athaiya. Activation functions in neural networks. International Journal of Engineering Applied Sciences and Technology, 4(12):310–316, 2020.

[22] J. J. Siang. Jaringan Syaraf Tiruan dan Pemrogramannya Menggunakan MATLAB, volume 2. 2009.

[23] P. G. Zhang. Time series forecasting using a hybrid arima and neural network model. Neurocomputing, 50:159–175, 2003.

[24] S. Kim and H. Kim. Anewmetricofabsolute percentage error for intermittent demand forecasts. International Journal of Forecasting, 32(3):669–679, 2016