Integrating VAR and CNN Models for Accurate Forecasting of Money Supply in Indonesia

Article Sidebar

Main Article Content

Abstract

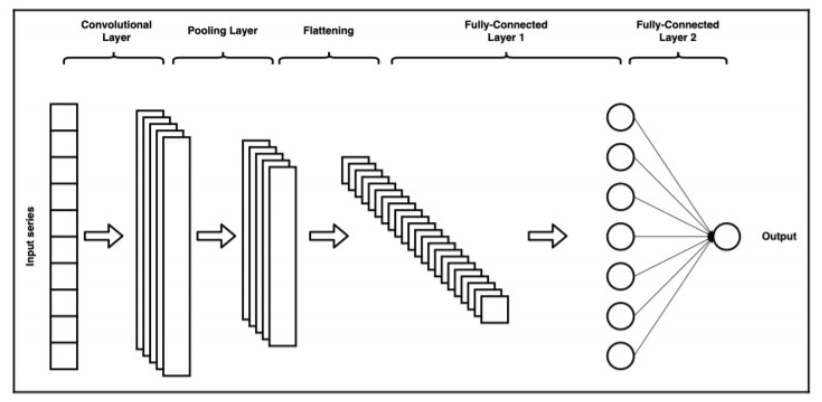

Economic forecasting serves as a fundamental element in supporting decision-making processes across multiple sectors. One of the main areas of interest in this field is the estimation of the money supply within an economy. The Vector Autoregressive (VAR) model is a commonly applied method for forecasting; however, it often encounters limitations when processing data with nonlinear patterns. Convolutional Neural Networks (CNNs) offer an alternative approach, particularly effective in identifying nonlinear structures that are not adequately captured by VAR models. A hybrid VAR-CNN model is therefore proposed, combining the respective strengths of both techniques to improve the accuracy of predictions. This research applies to the hybrid VAR-CNN model to forecast economic variables for the period from July 2022 to June 2023. The model consists of two main components: the first utilizes forecasted values generated by the VAR model, while the second processes the residuals from the VAR output using a CNN. With 80% of the data allocated for training and 20% for testing, the hybrid VAR-CNN model demonstrates improved performance over alternative forecasting methods. Evaluation based on Mean Absolute Percentage Error (MAPE), supremum (D) values, and p-values confirms the effectiveness of this hybrid approach.